HQ BLOG

HOME QUALIFIED BLOG

HQ INSIDER NEWS

Thursday, April 11, 2024 By: Ralph dibugnara Updated March 28, 2024 12:26 pm ET By Aly J. Yale https://www.wsj.com/buyside/personal-finance/mortgage-rates-01662579229 If you’re financing a home with a mortgage, ensuring you get the best possible rate is one of the smartest financial moves you can make. While it takes some legwork, the pay off is hard to argue with. Shaving even a fraction of a point from your rate can save you hundreds of dollars each month and tens of thousands over the life of the loan. For example, with a $400,000 mortgage, dropping from a 7% to a 6.5% rate would save you almost $50,000 in interest over a 30-year term—roughly enough to pay for a year of private college. Mortgage rates change constantly—and differ across mortgage companies . Here’s how to take advantage of those facts, compare current mortgage rates and get the best deal. Current mortgage rates: How high are average mortgage rates right now? For weeks now, average mortgage rates held steady in the high-6% range, according to Freddie Mac. As of the close of March, the average 30-year mortgage rate was 6.79%. Weekly mortgage rates WEEK ENDING AVERAGE 30-YEAR FIXED RATE AVERAGE 15-YEAR FIXED RATE March 28, 2024 6.79% 6.11% Mar. 21, 2024 6.87% 6.21% Mar. 13, 2024 6.74% 6.16% Mar. 7, 2024 6.88% 6.22% Feb. 29, 2024 6.94% 6.26% Freddie Mac “There has been a little more volatility since February, with rates moving up a bit—but they’re still below their highs from 2023,” says Rick Mount, managing partner of the Southwest region of Churchill Mortgage. Mount’s referring to last October, when rates nearly topped 8%. Still, average rates are about half a percentage point higher than they were a year ago—and borrowers have taken note. Applications for mortgages to purchase a new home are now down 16% compared to last year, according to the Mortgage Bankers Association. Refinances have dropped 9%. Where are mortgage rates headed? AVERAGE RATE DATE Current rate 6.79% March 28, 2024 This time last year 6.32% March 30, 2023 Highest point in last decade 7.79% Oct. 26, 2023 All-time high 18.53% Oct. 16, 1981 All-time low 2.65% Jan 7, 2021 Freddie Mac Mortgage rates have remained high thanks to stubborn inflation. Going into 2024, the Fed indicated lower rates may be on the horizon, but with inflation still sitting above the Federal Reserve’s 2% goal, those have yet to come to fruition. Instead, the Fed has kept interest rates elevated at its last several meetings, in an effort to bring inflation and consumer spending closer to its goal. “Inflation has continued to trend higher,’ says Ralph DiBugnara, a mortgage broker and senior vice president at Cardinal Financial, a mortgage company in Edgewater, N.J. “As long as inflation stays high or rises, the Fed will be hesitant to cut rates.” To be fair: The Fed doesn’t directly set mortgage rates, though they do tend to move in the same direction as the short-term rates it does control. As to when those rates might start to drop, it’s hard to say. Inflation notched up slightly in February, clocking in at 3.2%. “I believe the reality is we may see two to three cuts this year, all depending on inflation readings,” Mount says. “The Fed is committed to a 2% inflation rate, and I don’t expect we see meaningful cuts until that number is a reality.” According to the CME Group FedWatch Tool, which uses investing activity to predict future Fed moves, the Fed will likely hold steady on rates in May, with higher chances of rate cuts by the end of summer. MBA currently projects mortgage rates will drop to 6.3% by the end of the third quarter and 6.1% by year’s end. Fannie Mae predicts a 6.6% and 6.4% average, respectively. How are mortgage rates set? While the Fed influences mortgage rates, it is only one piece of the puzzle. Other external factors play a role, too—as do the details of your financial situation and loan choice. Here’s what you need to know about what determines your mortgage rate. External factors The overall state of the economy is a big contributor to the path of mortgage rates. When the economy is strong, rates tend to be higher. When the economy sputters, rates drop. “Interest rates often will rise or fall based on the strength of the economy, and ironically, bad news can be good news for lower interest rates,” says Bill Banfield, an executive at lender Rocket Mortgage. This is due in part to how economic conditions impact investment activity. When there are geopolitical concerns or the economy is wavering, investors tend to flock to safer investments—which include things such as Treasury bonds and mortgage-backed securities. This pushes the yields on those securities down (yields fall when bond prices rise), taking mortgage rates down with them. “When there is high demand for mortgage-backed securities, the prices of those MBS increase, which in turn can lower mortgage interest rates,” says Tanya Blanchard, founder of mortgage brokerage Madison Chase Capital Advisors. “This is because investors are willing to accept lower returns on their investments when the prices of MBS are high.” Finally, inflation factors in, too—and not just because of the Fed reaction. It also increases the costs for lenders to originate loans, which drives their prices higher as well. Personal factors Your personal finances will factor into your interest rate as well. First, there’s your credit score . Mortgage lenders use this number to gauge your risk as a borrower—or how likely you are to default on your loan. The lower your score, the higher the rate you’ll need to pay to compensate for the perceived risk. “Credit score is a very important consideration when applying for a mortgage,” Banfield says. “If someone has a proven track record of being responsible with their finances, they’ll be more likely to get a mortgage and a better rate.” The size of your down payment is important, too. A larger down payment means you have more to lose, which hopefully discourages you from defaulting. Smaller down payments, on the other hand, mean more risk for the lender and higher rates for you as a result. Loan-specific factors Last but not least, the type of mortgage loan you choose will also influence your rate. Loans backed by the government, such as Federal Housing Administration-backed FHA loans and Veterans Affairs-backed VA loans, tend to have lower rates than conventional or jumbo loans since they come with the federal government’s protection. Shorter-term loans (15 years, for example) also have lower rates than longer-term ones (30 years). As Goodwin explains, “While a shorter-term loan will come with a higher monthly payment, it could save you thousands on interest in the long run.” How, when and why to compare mortgage rates from different lenders Because every lender has different overhead costs, operating capacities and appetite for risk, mortgage rates can vary significantly from one company to the next. That’s why it’s important to consider several lenders before choosing where to get your loan. Freddie Mac recommends getting at least four quotes (it could save you an average of $1,200 a year , apparently). Just make sure you’re not only going by the rates a lender advertises on their website or on third-party sites. “Looking at advertised rates alone is not a good way to shop around,” Goodwin says. “Lenders typically display the lowest rates they offer as a headline to attract leads, but the actual rate you may be offered can vary dramatically depending on your own financial situation and the kind of loan you’re looking for.” Many advertised rates also include mortgage points —meaning you would need to pay an extra upfront fee to snag it. To get a rate that is truly a reflection of what you would pay as a borrower, you need to apply for preapproval . You’ll have to fill out an application and agree to a credit check for this. Once you’re done, you’ll get a loan estimate that will detail the total loan amount you are likely to qualify for, plus your interest rate and expected closing costs—or the fees required to originate, underwrite and close on your loan. Be sure to look at the APR, too—the annual percentage rate. This reflects the total annual cost of the loan, considering both your rate and any fees. Be warned, though: The rates you’re quoted aren’t guaranteed until you lock your rate. A rate lock guarantees your interest rate for a set period—usually only 30 to 60 days, depending on the lender. You’ll typically do this once you’ve found a home and have a contract in place. How to calculate your mortgage costs Comparing mortgage offers might seem tedious, but financially, it’s usually worthwhile. Even a small change in rate can have a big impact on your monthly payment and long-term interest costs. You can use a mortgage calculator to break down the exact costs or use your loan estimate. This should detail your monthly payment, your interest rate and your total interest paid in five years. See the difference that incremental rate changes can make on the cost of a 30-year, $400,000 home loan below: RATE MONTHLY PAYMENT INTEREST OVER 30 YEARS 5% $2,147 $373,023 5.25% $2,208 $395,173 5.50% $2,271 $417,616 5.75% $2,334 $440,344 6% $2,398 $463,352 6.25% $2,462 $486,632 6.50% $2,528 $510,177 6.75% $2,594 $533,981 7% $2,661 $558,035 Keep in mind that most mortgage loans are amortized, meaning the total costs are calculated and then paid in even payments across the loan term. With these loans, you’ll pay more interest upfront and less toward the end of the term. For example, your first payment at 6% would see $2,000 go toward interest, while your final payment would have just $11.93. “At the beginning of the loan term, the majority of the monthly payment will go toward interest,” says Colleen Bara, a lending executive with Key Bank. “As the loan is paid down, more of the monthly payment is allocated toward the pay-down of the principal balance.” This means if you sell your home quickly after taking out your loan, you likely won’t have paid down your balance much—and may not make much from the home, profit-wise. If this is a concern, making an extra payment each year you’re in the house can help. “Make one extra principal payment yearly and you can shave off approximately seven years of interest,” Blanchard says.

Thursday, April 11, 2024 By: Ralph dibugnara Updated March 28, 2024 12:26 pm ET By Aly J. Yale https://www.wsj.com/buyside/personal-finance/mortgage-rates-01662579229 If you’re financing a home with a mortgage, ensuring you get the best possible rate is one of the smartest financial moves you can make. While it takes some legwork, the pay off is hard to argue with. Shaving even a fraction of a point from your rate can save you hundreds of dollars each month and tens of thousands over the life of the loan. For example, with a $400,000 mortgage, dropping from a 7% to a 6.5% rate would save you almost $50,000 in interest over a 30-year term—roughly enough to pay for a year of private college. Mortgage rates change constantly—and differ across mortgage companies . Here’s how to take advantage of those facts, compare current mortgage rates and get the best deal. Current mortgage rates: How high are average mortgage rates right now? For weeks now, average mortgage rates held steady in the high-6% range, according to Freddie Mac. As of the close of March, the average 30-year mortgage rate was 6.79%. Weekly mortgage rates WEEK ENDING AVERAGE 30-YEAR FIXED RATE AVERAGE 15-YEAR FIXED RATE March 28, 2024 6.79% 6.11% Mar. 21, 2024 6.87% 6.21% Mar. 13, 2024 6.74% 6.16% Mar. 7, 2024 6.88% 6.22% Feb. 29, 2024 6.94% 6.26% Freddie Mac “There has been a little more volatility since February, with rates moving up a bit—but they’re still below their highs from 2023,” says Rick Mount, managing partner of the Southwest region of Churchill Mortgage. Mount’s referring to last October, when rates nearly topped 8%. Still, average rates are about half a percentage point higher than they were a year ago—and borrowers have taken note. Applications for mortgages to purchase a new home are now down 16% compared to last year, according to the Mortgage Bankers Association. Refinances have dropped 9%. Where are mortgage rates headed? AVERAGE RATE DATE Current rate 6.79% March 28, 2024 This time last year 6.32% March 30, 2023 Highest point in last decade 7.79% Oct. 26, 2023 All-time high 18.53% Oct. 16, 1981 All-time low 2.65% Jan 7, 2021 Freddie Mac Mortgage rates have remained high thanks to stubborn inflation. Going into 2024, the Fed indicated lower rates may be on the horizon, but with inflation still sitting above the Federal Reserve’s 2% goal, those have yet to come to fruition. Instead, the Fed has kept interest rates elevated at its last several meetings, in an effort to bring inflation and consumer spending closer to its goal. “Inflation has continued to trend higher,’ says Ralph DiBugnara, a mortgage broker and senior vice president at Cardinal Financial, a mortgage company in Edgewater, N.J. “As long as inflation stays high or rises, the Fed will be hesitant to cut rates.” To be fair: The Fed doesn’t directly set mortgage rates, though they do tend to move in the same direction as the short-term rates it does control. As to when those rates might start to drop, it’s hard to say. Inflation notched up slightly in February, clocking in at 3.2%. “I believe the reality is we may see two to three cuts this year, all depending on inflation readings,” Mount says. “The Fed is committed to a 2% inflation rate, and I don’t expect we see meaningful cuts until that number is a reality.” According to the CME Group FedWatch Tool, which uses investing activity to predict future Fed moves, the Fed will likely hold steady on rates in May, with higher chances of rate cuts by the end of summer. MBA currently projects mortgage rates will drop to 6.3% by the end of the third quarter and 6.1% by year’s end. Fannie Mae predicts a 6.6% and 6.4% average, respectively. How are mortgage rates set? While the Fed influences mortgage rates, it is only one piece of the puzzle. Other external factors play a role, too—as do the details of your financial situation and loan choice. Here’s what you need to know about what determines your mortgage rate. External factors The overall state of the economy is a big contributor to the path of mortgage rates. When the economy is strong, rates tend to be higher. When the economy sputters, rates drop. “Interest rates often will rise or fall based on the strength of the economy, and ironically, bad news can be good news for lower interest rates,” says Bill Banfield, an executive at lender Rocket Mortgage. This is due in part to how economic conditions impact investment activity. When there are geopolitical concerns or the economy is wavering, investors tend to flock to safer investments—which include things such as Treasury bonds and mortgage-backed securities. This pushes the yields on those securities down (yields fall when bond prices rise), taking mortgage rates down with them. “When there is high demand for mortgage-backed securities, the prices of those MBS increase, which in turn can lower mortgage interest rates,” says Tanya Blanchard, founder of mortgage brokerage Madison Chase Capital Advisors. “This is because investors are willing to accept lower returns on their investments when the prices of MBS are high.” Finally, inflation factors in, too—and not just because of the Fed reaction. It also increases the costs for lenders to originate loans, which drives their prices higher as well. Personal factors Your personal finances will factor into your interest rate as well. First, there’s your credit score . Mortgage lenders use this number to gauge your risk as a borrower—or how likely you are to default on your loan. The lower your score, the higher the rate you’ll need to pay to compensate for the perceived risk. “Credit score is a very important consideration when applying for a mortgage,” Banfield says. “If someone has a proven track record of being responsible with their finances, they’ll be more likely to get a mortgage and a better rate.” The size of your down payment is important, too. A larger down payment means you have more to lose, which hopefully discourages you from defaulting. Smaller down payments, on the other hand, mean more risk for the lender and higher rates for you as a result. Loan-specific factors Last but not least, the type of mortgage loan you choose will also influence your rate. Loans backed by the government, such as Federal Housing Administration-backed FHA loans and Veterans Affairs-backed VA loans, tend to have lower rates than conventional or jumbo loans since they come with the federal government’s protection. Shorter-term loans (15 years, for example) also have lower rates than longer-term ones (30 years). As Goodwin explains, “While a shorter-term loan will come with a higher monthly payment, it could save you thousands on interest in the long run.” How, when and why to compare mortgage rates from different lenders Because every lender has different overhead costs, operating capacities and appetite for risk, mortgage rates can vary significantly from one company to the next. That’s why it’s important to consider several lenders before choosing where to get your loan. Freddie Mac recommends getting at least four quotes (it could save you an average of $1,200 a year , apparently). Just make sure you’re not only going by the rates a lender advertises on their website or on third-party sites. “Looking at advertised rates alone is not a good way to shop around,” Goodwin says. “Lenders typically display the lowest rates they offer as a headline to attract leads, but the actual rate you may be offered can vary dramatically depending on your own financial situation and the kind of loan you’re looking for.” Many advertised rates also include mortgage points —meaning you would need to pay an extra upfront fee to snag it. To get a rate that is truly a reflection of what you would pay as a borrower, you need to apply for preapproval . You’ll have to fill out an application and agree to a credit check for this. Once you’re done, you’ll get a loan estimate that will detail the total loan amount you are likely to qualify for, plus your interest rate and expected closing costs—or the fees required to originate, underwrite and close on your loan. Be sure to look at the APR, too—the annual percentage rate. This reflects the total annual cost of the loan, considering both your rate and any fees. Be warned, though: The rates you’re quoted aren’t guaranteed until you lock your rate. A rate lock guarantees your interest rate for a set period—usually only 30 to 60 days, depending on the lender. You’ll typically do this once you’ve found a home and have a contract in place. How to calculate your mortgage costs Comparing mortgage offers might seem tedious, but financially, it’s usually worthwhile. Even a small change in rate can have a big impact on your monthly payment and long-term interest costs. You can use a mortgage calculator to break down the exact costs or use your loan estimate. This should detail your monthly payment, your interest rate and your total interest paid in five years. See the difference that incremental rate changes can make on the cost of a 30-year, $400,000 home loan below: RATE MONTHLY PAYMENT INTEREST OVER 30 YEARS 5% $2,147 $373,023 5.25% $2,208 $395,173 5.50% $2,271 $417,616 5.75% $2,334 $440,344 6% $2,398 $463,352 6.25% $2,462 $486,632 6.50% $2,528 $510,177 6.75% $2,594 $533,981 7% $2,661 $558,035 Keep in mind that most mortgage loans are amortized, meaning the total costs are calculated and then paid in even payments across the loan term. With these loans, you’ll pay more interest upfront and less toward the end of the term. For example, your first payment at 6% would see $2,000 go toward interest, while your final payment would have just $11.93. “At the beginning of the loan term, the majority of the monthly payment will go toward interest,” says Colleen Bara, a lending executive with Key Bank. “As the loan is paid down, more of the monthly payment is allocated toward the pay-down of the principal balance.” This means if you sell your home quickly after taking out your loan, you likely won’t have paid down your balance much—and may not make much from the home, profit-wise. If this is a concern, making an extra payment each year you’re in the house can help. “Make one extra principal payment yearly and you can shave off approximately seven years of interest,” Blanchard says.

Thursday, April 4, 2024 By: Ralph dibugnara By: Erik J. Martin Reviewed By: Aleksandra Kadzielawski March 26, 2024 - 9 min read https://themortgagereports.com/111388/what-will-the-2024-spring-homebuying-season-look-like With the weather warming up and flowers starting to bloom, it’s natural to get excited about the spring season upon us. But will hope spring eternal for home shoppers and sellers alike over the next few months? What’s in store for us as the national spring home buying season begins? When in doubt, consult those in the know. So we contacted several trusted housing market experts for their analyses and forecasts about the spring home buying season, including predictions on mortgage rates , home prices, and inventory as well as tips on how house hunters can get a leg up on the competition. What will the 2024 spring homebuying season look like? With the arrival of spring, many eyes turn towards the real estate market, particularly for individuals aspiring to buy a home. Here’s how industry insiders expect the spring home buying season to shake out, in general. Check your home buying options. Start here (Mar 26th, 2024) Albert Lord , founder/CEO of Lexerd Capital Management: “Housing affordability remains a significant concern, with high home prices and mortgage rates posing challenges for buyers. The ongoing shortage of housing supply, coupled with robust demand, is expected to sustain high home prices this season. And mortgage rates are expected to play a pivotal role in the spring market, too. The recent decline in mortgage rates is anticipated to incentivize buyer activity this spring, and the Federal Reserve’s indication of potential rate cuts in 2024 adds further encouragement. Political factors, including government policies and the upcoming elections, are also likely to affect the housing market. President Biden’s administration has already introduced initiatives to enhance housing affordability , which could include subsidizing down payments and promoting inclusionary zoning.” Rick Sharga , president/CEO of CJ Patrick Company: “The Fed’s actions have caused mortgage rates to soar, making affordability a problem for buyers and making it economically impossible for many homeowners to sell their homes and buy a new one with a mortgage rate twice as high as their current loan. So even though we are likely to see a slight seasonal uptick in property listings, we are not likely to see much more than a modest year-over-year increase in existing home sales. We’re locked into a cycle with limited supply, pent-up demand, high financing costs, and poor affordability. If we see the typical surge in demand that usually happens in the spring without a commensurate increase in supply, we will probably see sales numbers similar to last year’s lackluster totals, and prices will tick up a bit.” Mike Hardy , managing partner at Churchill Mortgage: “If we step back and look at this from a 30,000-foot perspective, we have a basic supply and demand issue, as there are significantly more people who need homes than inventory can support. Additionally, new builds are not projected to keep up with the incoming population. Inflation trends will be the key driver this spring, which will directly impact mortgage rates. Higher inflation – and subsequently higher mortgage rates – could cause a slowdown of buyers, with inventory creeping up slightly. On the other hand, falling inflation will likely cause mortgage rates to trend downward , bringing more buyers into the market and creating a bit of a frenzy with multiple offers in many areas where inventory levels are currently much lower than the historical average.” Dennis Shirshikov , adjunct professor of economics at City University of New York: “The spring market is likely to be driven by a mix of lingering economic recovery signals, environmental considerations, and the political climate. Economic factors such as inflation rates, employment figures, and consumer spending will play critical roles as well. Keep in mind that environmental concerns – including sustainability and energy efficiency – are increasingly influencing buyer preferences. Politically, regulatory changes and fiscal policies will affect market dynamics. Overall, I predict a season characterized by cautious optimism among buyers , with a keen eye on value and sustainability.” Will home prices fall this spring? With spring around the corner, hopeful homebuyers are curious: will prices finally ease up? Keeping an eye on market shifts is pivotal for those eyeing their dream homes. Let’s hear real estate experts’ take on whether prices will soften this season. Check your home buying options. Start here (Mar 26th, 2024) Dave Liniger , chairman of RE/MAX: “I don’t believe there will be a significant decline in home prices throughout the United States this spring. It will be dependent on specific regions, whereas there is still tremendous demand in certain areas and less demand in others.” Martin Orefice , CEO of Rent To Own Labs: “Housing prices may start creeping a bit lower this spring, but they aren’t going to drop so far that they change the fundamental dynamic. Homes, especially starter properties, will remain unaffordable, especially to first-time buyers.” Ralph DiBugnara , president of Home Qualified: “I believe we will see a trend upward in home prices. With a continued shortage of real estate for sale in most states, prices overall have nowhere to go but up because of lack of supply and high demand.” Lord: “I believe home prices will rise by 2% this spring, given the imbalances in supply and demand. The prevailing sentiment seems to be that, while prices will continue to rise, the pace of appreciation will slow down. This moderation in price growth is expected to vary across regions, with some markets experiencing price declines. The National Association of Realtors predicts a 1.4% increase in median prices, while Fannie Mae’s forecast estimates an average home price growth of 3.8% across 2024 .” Hardy: “I expect to see home prices rise over the next few months. There are simply more buyers that need and want housing than there are homes available for sale. We are seeing real-time reports of open houses with 50 to 100 people attending and multiple offers. It remains an absolute feeding frenzy in markets with low levels of inventory.” Sharga: “On a national basis, home prices are probably going to continue to increase in the 2024 spring buying season for two reasons. First, prices almost always peak during the spring and summer months, and this year isn’t likely to be any different. Second, demand also tends to peak during this period and is expected to overwhelm the limited supply of homes available for sale.” Will mortgage interest rates drop this season? As the spring home buying season approaches, prospective buyers and homeowners eagerly anticipate shifts in mortgage rates, which can significantly impact the affordability and dynamics of the real estate market. Find your lowest mortgage rate. Start here (Mar 26th, 2024) Here are insights from real estate experts on whether they predict mortgage rates to drop: Hardy: “Rates will likely trend down over the next 12 months, but expect some volatility. Mortgage rates have historically moved in tandem and track with inflation. Each time interest rates have dropped by 1%, roughly five million additional people have been able to afford a home that previously could not qualify. So if rates drop from the current territory of about 6.75% to 5.75%, I expect we will have approximately five million more people who can purchase a home this spring.” Jason Gelios , a Realtor in Southeast Michigan: “Mortgage rates should trend lower this season, with the rumor of the Federal Reserve decreasing the rate twice this year. While we won’t see mortgage rates drop to the 2% to 3% range anytime soon, we will see some relief in the spring to summer 2024 homebuying season.” Lord: “I foresee modest declines in mortgage rates, with the 30-year mortgage rate averaging 6.9% this spring. What will drive rate declines is not so much the current interest rate climate but the expectation for future declines in interest rates based on the Fed’s data-dependent analysis.” Shirhikov: “Mortgage rates are expected to fluctuate this season. Should the Fed decide to cut rates to stimulate the economy, we could see a temporary dip, making the spring buying season more attractive. However, buyers should remain vigilant, as rates are subject to rapid changes based on broader economic signals.” What will inventory look like over the next few months? The availability of homes for sale plays a crucial role in shaping market dynamics and influencing buyer decisions. Here are insights from real estate experts regarding their predictions for home inventory this spring: Check your home buying options. Start here (Mar 26th, 2024) Liniger: “Presently, there is a significant demand for residential property driven by younger generations like Millennials and Generation Z, who dominate the market and account for 50% of the current workforce. However, despite a tremendous number of buyers, insufficient inventory remains a challenge. There probably won’t be much change over the next three months unless there is interest rate assistance from the government. Younger generations who have become used to previous lower interest rates at 2.5% to 5% will also eventually come to terms with current interest rates sitting at 7% to 8%.” Hardy: “I anticipate a slight rise in inventory in the short term. As rates get noticeably lower and into the 5% range, this supply trend will change, as another wave of buyers will enter the market and we will see inventory start to drop.” Shirshikov: “Inventory levels are anticipated to slightly increase in certain areas, driven by new construction and sellers entering the market to capitalize on stable prices. However, overall supply will likely remain tight, continuing the trend of a seller’s market in many areas. This scarcity underpins the importance of strategic buying and selling decisions.” Orefice: “Inventory will remain too low to meet demand, especially in pricey urban and suburban markets, although some new construction – especially of apartments – may take the edge off.” Sharga: “Supply is likely to increase during the spring, coming off near-record lows from a year ago. This increase might be a little misleading, as it’s only partly due to a bump in new listings and also partly because it’s taking a bit longer to sell properties once they are listed. Even with this seasonal increase, we may still have somewhere between 30% and 40% fewer homes available for sale than we did before the pandemic. On the other hand, we should continue to see an increase in the number of new homes for sale, as January building permits increased by 8.6% from January 2023, and single-family housing starts were up as well.” Tactics buyers can take for better success this spring As we gear up for the spring home buying season, it’s vital for aspiring homeowners to adopt smart strategies to boost their chances of finding their dream home. Here’s some friendly advice from real estate experts sharing tactics to help you navigate the market and enhance your prospects this spring: Time to make a move? Let us find the right mortgage for you (Mar 26th, 2024) Shishikov: “Shoppers can adapt several unique strategies to enhance their chances of securing a desired home. Explore off-market properties, leverage technology for virtual tours and faster decision-making, and consider alternative financing options. Engaging with a real estate professional who has a deep understanding of specific local markets can also provide a competitive edge. Above all, remain adaptable, informed, and ready to act decisively.” Hardy: “I suggest 10 ways that can help buyers get an offer accepted this spring. First, get fully approved for a mortgage before you make an offer. Second, work with a reputable real estate agent. Third, make an offer above the asking price. Fourth, be flexible with the closing date. Fifth, limit or waive any contingencies in your offer. Sixth, use an escalation clause in your offer. Seventh, offer to cover certain seller expenses. Eight, increase your earnest money deposit. Ninth, offer a $10,000 performance guarantee. And tenth, have your lender or agent send a personal video or letter from you to the seller to stand out from other buyers.” Orefice: “If there’s a home you are really after, you need to be prepared to make an offer over the asking price or, better yet, a cash offer.” DiBugnara: “Homes that need TLC are going to be among the only value buys right now. If you can find a home that has manageable repairs, it’s best to go that route. There are more renovation loans available today that can help with this process.” The bottom line The experts agree: A variety of economic, political, environmental, and unpredictable factors will drive the 2024 spring homebuying season. Of course, many of these elements are out of your control. Still, you can put yourself in a better position to find, afford, and close on a desirable home for sale this spring by doing your homework, learning about market conditions, making preparations as early as possible, and partnering with a seasoned real estate professional.

Thursday, Mar 28, 2024 By: Ralph dibugnara By: Paul Centopani February 29, 2024 Mortgage rate forecast for next week (March 4-8) Mortgage rates reached a two-month high, growing for the fourth straight week. The average 30-year fixed rate mortgage (FRM) increased from 6.9% on Feb. 22 to 6.94% on Feb. 29, according to Freddie Mac. “The recent boomerang in rates has dampened already tentative homebuyer momentum as we approach the spring, a historically busy season for home buying,” said Sam Khater, Freddie Mac’s chief economist. “While sales of newly built homes are trending in a positive direction, higher rates and elevated prices continue to pose affordability challenges that may leave potential homebuyers on the sidelines.” Will mortgage rates go down in March? Mortgage rates fluctuated significantly in 2023, with the average 30-year fixed rate going as low as 6.09% on Feb. 2 and as high as 7.79% on Oct. 26, according to Freddie Mac. Find your lowest mortgage rate. Start here (Feb 29th, 2024) The range can be largely attributed to the Federal Reserve’s ongoing fight against inflation, juxtaposed with uncertainty in the banking sector sparked by Silicon Valley Bank’s collapse. However, with duress permeating the financial market and the fallout from U.S. debt ceiling talks, the Fed may continue making hikes to bring interest rates down. With the economy possibly heading into a recession, we may have already seen the peak of this rate cycle. Of course, interest rates are notoriously volatile and could tick back up on any given week. Experts from CoreLogic, Home Qualified, Realtor.com and others weigh in on whether 30-year mortgage rates will climb, fall, or level off in March. Expert mortgage rate predictions for March Craig Berry , branch manager at Acopia Home Loans Prediction: Rates will moderate “In their Jan. 31 meeting, the Fed opted to leave rates alone. According to the Federal Reserve, inflation is coming down faster than expected due to “a robust economy”. Even so, the Fed indicated they’ll need to see additional indicators that inflation has stabilized prior to making any rate cuts. This news didn’t help mortgage rates. Other than slight fluctuations, rates will remain relatively flat through the month of March.” Molly Boesel , principal economist at CoreLogic Prediction: Rates will moderate “The Federal Reserve has taken a pause on interest rates as they monitor inflation, and those looking for decreases in rates will need to be patient. When inflation approaches the Fed target, rates should start to decrease. Until then, look for the 30-year mortgage rate to be in the high-6% range in March.” Ralph DiBugnara , president at Home Qualified Prediction: Rates will rise “So far, the first quarter of 2024 has been very similar to the first quarter of 2023. Inflation has been up in some categories and made rates move more upward than downward. Rates came down at the end of 2023 but the most recent Fed meeting should sign that there won’t be any rate cuts until summer 2024. I believe that lack of commitment to cut or raise by the Fed will keep the market guessing and we will see averages creep up some. The 30-year fixed rate will average 7.25% in March while the 15-year fixed will average 6.75%.” Selma Hepp , chief economist at CoreLogic Prediction: Rates will moderate “The US economy continues to show signs of strength, so therefore, rates are likely to remain stable through the spring home buying season, with cuts not expected until the beginning of summer. However, in recent industry surveys, home buyers are beginning to feel optimistic about where rates are heading and more and more home buyers are anticipating rates to decline through the year.” Hannah Jones , senior economic research analyst at Realtor.com Prediction: Rates will moderate “Mortgage rates are likely to remain steady through March, dependent on incoming economic data. At the February FOMC meeting, Chair Powell emphasized that it is unlikely that we will see a rate cut in March as incoming economic data remains fairly strong. Later the same week, January employment data came in well above expectation with the economy adding 353,000 net new jobs in the month. The still-strong employment data demonstrated that slowing the economy may not be a straight path, and prolonged contractionary policy may be necessary. Mortgage rates are likely to remain in the mid to high 6% for the time being until slowing inflation shifts investor expectations and the Fed starts to cut interest rates.” Jess Kennedy , COO at Beeline Prediction: Rates will moderate “We predict that rates will hold relatively steady in March. The Fed has signaled pretty strongly that they are in a holding pattern right now. We may see slight fluctuations but generally, we don’t expect much movement. The 10-year bond and 30-year mortgage rate spread continues to be pretty large and we don’t anticipate that to change any time soon since the Federal Reserve is no longer buying MBS, so the demand for MBS is lower.” Odeta Kushi , deputy chief economist at First American Prediction: Rates will moderate “The average 30-year fixed mortgage rate has fallen in recent months, but ticked up again recently due to strong economic and labor market data. Initial optimism for Federal Reserve rate cuts was tempered after recent data, prompting the increase in mortgage rates. Traders have now ruled out a March rate cut , yet May could still see a reduction. This suggests potential mortgage rate volatility ahead, dependent on future economic data. Should this economic data exceed expectations, rates may rise further. Nonetheless, ongoing deceleration in inflation fuels cautious optimism for a general decline in mortgage rates in 2024, especially in the latter half of the year.” Rick Sharga , CEO at CJ Patrick Company Prediction: Rates will moderate “The consensus is that the Federal Reserve will hold steady at its March meeting, neither raising nor cutting the Fed Funds Rate. Mortgage rates on 30-year fixed rate loans in March will likely do the same, neither rising or declining very much, staying in a fairly narrow band between 6.5-7.0%, fluctuating with reports on various economic metrics. The sudden dip in rates in the month of January appears to have been an overreaction by the market to language from the Fed that was interpreted as a sign of rate cuts as early as the first quarter. With that increasingly unlikely to happen, we’ve seen mortgage rates inch back up, and are likely to see them zig zag in a gradually downward direction for the rest of the year, but not drop meaningfully until the first rate cut by the Fed actually happens.” Charles Williams , CEO at Percy Prediction: Rates will moderate “In a recent interview on 60 Minutes, Fed Chair Jerome Powell gave a strong indication that they won’t be cutting rates before the economy hits the target rates of 2%. With jobs numbers still very strong, it’s not likely we’ll see a rate cut until March, perhaps even May. And even then, it will be a slow and gradual pullback, so we’ll be lucky to dip below 6% mortgage rates by the end of the year.”

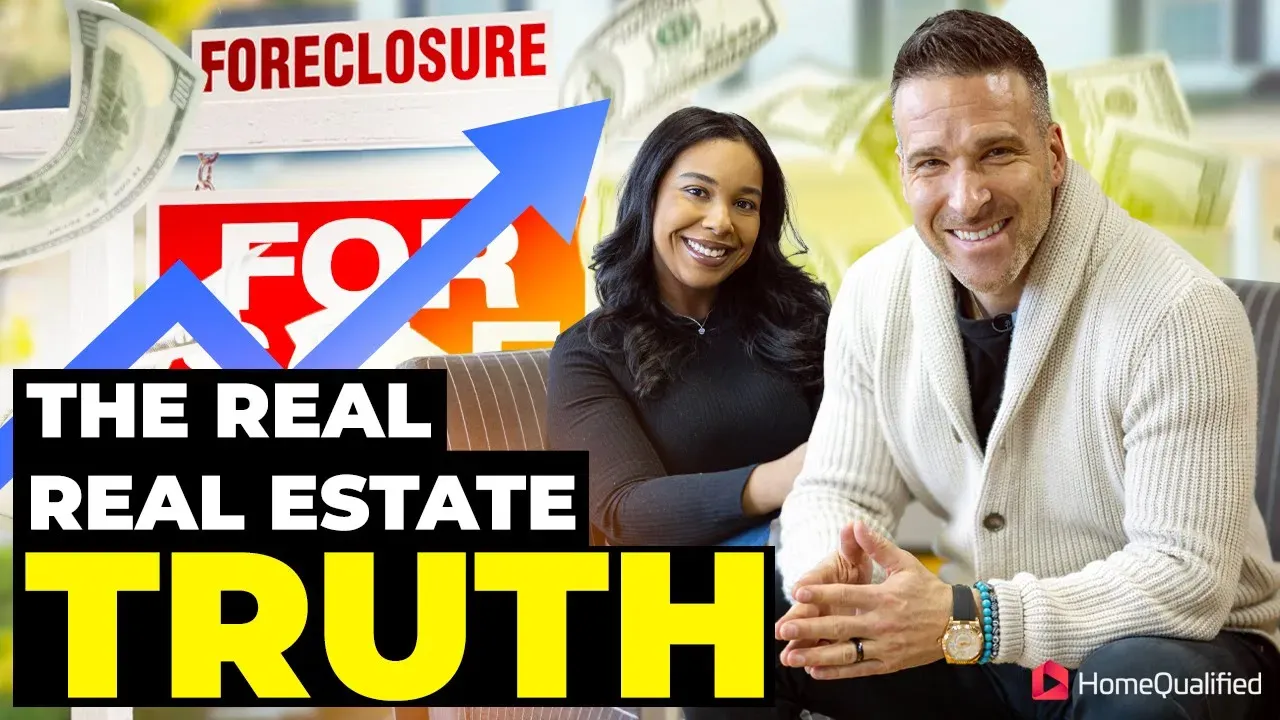

Debunking Real Estate Myths: The Real Real Estate Truths In today's special segment, "The Real Real Estate Truths," Ralph and Keyla , will unravel some of the trending speculations circulating on social media over the past few months and provide you with the real facts about the real estate market.

Demystifying Real Estate Investment: The Accredited Investor, Cash Flow Realities, and Mortgage Insights In this episode we will delve into the intricacies of real estate investment, debunking myths, and providing valuable insights for both seasoned investors and those looking to enter the market.

The Real Real Estate Truths Welcome to Home Qualified News, where we bring you the latest insights into the real estate market. In today's special segment, "The Real Real Estate Truth," Ralph DiBugnara and Keyla Rosario delve into recent social media trends to separate fact from fiction.

Friday, Mar 1, 2024 By: Ralph dibugnara By Kristine Hansen Feb 28, 2024 When you apply for a mortgage or refinance an existing mortgage, you want to secure the lowest interest rate possible. Any opportunity a borrower can exploit to shave dollars off the cost is a big win. This explains the allure of no-fee mortgages. These home loans and their promise of doing away with pesky fees always sound appealing—a lack of lender fees or closing costs is sweet music to a borrower’s ears. However, they come with their own set of pros and cons. No-fee mortgages have experienced a renaissance given the current economic climate, according to Ralph DiBugnara, president of Home Qualified . “No-fee programs are popular among those looking to refinance … [and] first-time home buyers [have] also increased as far as interest” goes. Be prepared for a higher interest rate But nothing is truly free, and this maxim applies to no-fee mortgages as well. They almost always carry a higher interest rate. “Over time, paying more interest will be significantly more expensive than paying fees upfront,” says DiBugnara. “If no-cost is the offer, the first question that should be asked is, ‘What is my rate if I pay the fees?’” Randall Yates, CEO of The Lenders Network , breaks down the math. “Closing costs are typically 2% to 5% of the loan amount,” he explains. “On a $200,000 loan, you can expect to pay approximately $7,500 in lender fees. Let’s say the interest rate is 4%, and a no-fee mortgage has a rate of 4.5%. [By securing a regular loan], you will save over $13,000 over the course of the loan.” So while you’ll have saved $7,500 in the short term, over the long term you’ll wind up paying more due to a higher interest rate. Weigh it out with your financial situation. Consider the life of the loan And before you start calculating the money that you think you might save with a no-fee mortgage, consider your long-term financial strategy. “No-fee mortgage options should only be used when a short-term loan is absolutely necessary,” says Jack Choros of CPI Inflation Calculator . A no-fee mortgage may be a smart tactic if you don’t plan to stay in one place for a long time or plan to refinance quickly. “If I am looking to move in a year or two, or think rates might be lower and I might refinance again, then I want to minimize my costs,” says Matt Hackett, operations manager at EquityNow . But “if I think I am going to be in the loan for 10 years, then I want to pay more upfront for a lower rate.” What additional fees should you be prepared to pay? As with any large purchase, whether it’s a car or computer, there’s no flat “this is it” price. Hidden costs always lurk in the fine print. “Most of the time, the cost for credit reports , recording fees, and flood-service fee are not included in a no-fee promise, but they are minimal,” says DiBugnara. “Also, the appraisal will always be paid by the consumer. They are considered a third-party vendor, and they have to be paid separately.” “All other costs such as property taxes, home appraisal, homeowners insurance, and private mortgage insurance will all still be paid by the borrower,” adds Yates. It’s important to ask what additional fees are required, as it varies from lender to lender, and state to state. The last thing you want is a huge surprise. “Deposits that are required to set up your escrow account, such as flood insurance, homeowners insurance, and property taxes, are normally paid at closing,” says Jerry Elinger, mortgage production manager at Silverton Mortgage in Atlanta. “Most fees, however, will be able to be covered by rolling them into the cost of the loan or paying a higher interest rate.” When does a no-fee mortgage make sense? For borrowers who want to save cash right now, but don’t mind paying more over a long time frame, a no-fee mortgage could be the right fit. “If your plan is long-term, it will almost always make more sense to pay the closing costs and take a lower rate,” says DiBugnara. “If your plan is short-term, then no closing costs and paying more interest over a short period of time will be more cost-effective.”

FEATURED ARTICLES

Thursday, April 11, 2024 By: Ralph dibugnara Updated March 28, 2024 12:26 pm ET By Aly J. Yale https://www.wsj.com/buyside/personal-finance/mortgage-rates-01662579229 If you’re financing a home with a mortgage, ensuring you get the best possible rate is one of the smartest financial moves you can make. While it takes some legwork, the pay off is hard to argue with. Shaving even a fraction of a point from your rate can save you hundreds of dollars each month and tens of thousands over the life of the loan. For example, with a $400,000 mortgage, dropping from a 7% to a 6.5% rate would save you almost $50,000 in interest over a 30-year term—roughly enough to pay for a year of private college. Mortgage rates change constantly—and differ across mortgage companies . Here’s how to take advantage of those facts, compare current mortgage rates and get the best deal. Current mortgage rates: How high are average mortgage rates right now? For weeks now, average mortgage rates held steady in the high-6% range, according to Freddie Mac. As of the close of March, the average 30-year mortgage rate was 6.79%. Weekly mortgage rates WEEK ENDING AVERAGE 30-YEAR FIXED RATE AVERAGE 15-YEAR FIXED RATE March 28, 2024 6.79% 6.11% Mar. 21, 2024 6.87% 6.21% Mar. 13, 2024 6.74% 6.16% Mar. 7, 2024 6.88% 6.22% Feb. 29, 2024 6.94% 6.26% Freddie Mac “There has been a little more volatility since February, with rates moving up a bit—but they’re still below their highs from 2023,” says Rick Mount, managing partner of the Southwest region of Churchill Mortgage. Mount’s referring to last October, when rates nearly topped 8%. Still, average rates are about half a percentage point higher than they were a year ago—and borrowers have taken note. Applications for mortgages to purchase a new home are now down 16% compared to last year, according to the Mortgage Bankers Association. Refinances have dropped 9%. Where are mortgage rates headed? AVERAGE RATE DATE Current rate 6.79% March 28, 2024 This time last year 6.32% March 30, 2023 Highest point in last decade 7.79% Oct. 26, 2023 All-time high 18.53% Oct. 16, 1981 All-time low 2.65% Jan 7, 2021 Freddie Mac Mortgage rates have remained high thanks to stubborn inflation. Going into 2024, the Fed indicated lower rates may be on the horizon, but with inflation still sitting above the Federal Reserve’s 2% goal, those have yet to come to fruition. Instead, the Fed has kept interest rates elevated at its last several meetings, in an effort to bring inflation and consumer spending closer to its goal. “Inflation has continued to trend higher,’ says Ralph DiBugnara, a mortgage broker and senior vice president at Cardinal Financial, a mortgage company in Edgewater, N.J. “As long as inflation stays high or rises, the Fed will be hesitant to cut rates.” To be fair: The Fed doesn’t directly set mortgage rates, though they do tend to move in the same direction as the short-term rates it does control. As to when those rates might start to drop, it’s hard to say. Inflation notched up slightly in February, clocking in at 3.2%. “I believe the reality is we may see two to three cuts this year, all depending on inflation readings,” Mount says. “The Fed is committed to a 2% inflation rate, and I don’t expect we see meaningful cuts until that number is a reality.” According to the CME Group FedWatch Tool, which uses investing activity to predict future Fed moves, the Fed will likely hold steady on rates in May, with higher chances of rate cuts by the end of summer. MBA currently projects mortgage rates will drop to 6.3% by the end of the third quarter and 6.1% by year’s end. Fannie Mae predicts a 6.6% and 6.4% average, respectively. How are mortgage rates set? While the Fed influences mortgage rates, it is only one piece of the puzzle. Other external factors play a role, too—as do the details of your financial situation and loan choice. Here’s what you need to know about what determines your mortgage rate. External factors The overall state of the economy is a big contributor to the path of mortgage rates. When the economy is strong, rates tend to be higher. When the economy sputters, rates drop. “Interest rates often will rise or fall based on the strength of the economy, and ironically, bad news can be good news for lower interest rates,” says Bill Banfield, an executive at lender Rocket Mortgage. This is due in part to how economic conditions impact investment activity. When there are geopolitical concerns or the economy is wavering, investors tend to flock to safer investments—which include things such as Treasury bonds and mortgage-backed securities. This pushes the yields on those securities down (yields fall when bond prices rise), taking mortgage rates down with them. “When there is high demand for mortgage-backed securities, the prices of those MBS increase, which in turn can lower mortgage interest rates,” says Tanya Blanchard, founder of mortgage brokerage Madison Chase Capital Advisors. “This is because investors are willing to accept lower returns on their investments when the prices of MBS are high.” Finally, inflation factors in, too—and not just because of the Fed reaction. It also increases the costs for lenders to originate loans, which drives their prices higher as well. Personal factors Your personal finances will factor into your interest rate as well. First, there’s your credit score . Mortgage lenders use this number to gauge your risk as a borrower—or how likely you are to default on your loan. The lower your score, the higher the rate you’ll need to pay to compensate for the perceived risk. “Credit score is a very important consideration when applying for a mortgage,” Banfield says. “If someone has a proven track record of being responsible with their finances, they’ll be more likely to get a mortgage and a better rate.” The size of your down payment is important, too. A larger down payment means you have more to lose, which hopefully discourages you from defaulting. Smaller down payments, on the other hand, mean more risk for the lender and higher rates for you as a result. Loan-specific factors Last but not least, the type of mortgage loan you choose will also influence your rate. Loans backed by the government, such as Federal Housing Administration-backed FHA loans and Veterans Affairs-backed VA loans, tend to have lower rates than conventional or jumbo loans since they come with the federal government’s protection. Shorter-term loans (15 years, for example) also have lower rates than longer-term ones (30 years). As Goodwin explains, “While a shorter-term loan will come with a higher monthly payment, it could save you thousands on interest in the long run.” How, when and why to compare mortgage rates from different lenders Because every lender has different overhead costs, operating capacities and appetite for risk, mortgage rates can vary significantly from one company to the next. That’s why it’s important to consider several lenders before choosing where to get your loan. Freddie Mac recommends getting at least four quotes (it could save you an average of $1,200 a year , apparently). Just make sure you’re not only going by the rates a lender advertises on their website or on third-party sites. “Looking at advertised rates alone is not a good way to shop around,” Goodwin says. “Lenders typically display the lowest rates they offer as a headline to attract leads, but the actual rate you may be offered can vary dramatically depending on your own financial situation and the kind of loan you’re looking for.” Many advertised rates also include mortgage points —meaning you would need to pay an extra upfront fee to snag it. To get a rate that is truly a reflection of what you would pay as a borrower, you need to apply for preapproval . You’ll have to fill out an application and agree to a credit check for this. Once you’re done, you’ll get a loan estimate that will detail the total loan amount you are likely to qualify for, plus your interest rate and expected closing costs—or the fees required to originate, underwrite and close on your loan. Be sure to look at the APR, too—the annual percentage rate. This reflects the total annual cost of the loan, considering both your rate and any fees. Be warned, though: The rates you’re quoted aren’t guaranteed until you lock your rate. A rate lock guarantees your interest rate for a set period—usually only 30 to 60 days, depending on the lender. You’ll typically do this once you’ve found a home and have a contract in place. How to calculate your mortgage costs Comparing mortgage offers might seem tedious, but financially, it’s usually worthwhile. Even a small change in rate can have a big impact on your monthly payment and long-term interest costs. You can use a mortgage calculator to break down the exact costs or use your loan estimate. This should detail your monthly payment, your interest rate and your total interest paid in five years. See the difference that incremental rate changes can make on the cost of a 30-year, $400,000 home loan below: RATE MONTHLY PAYMENT INTEREST OVER 30 YEARS 5% $2,147 $373,023 5.25% $2,208 $395,173 5.50% $2,271 $417,616 5.75% $2,334 $440,344 6% $2,398 $463,352 6.25% $2,462 $486,632 6.50% $2,528 $510,177 6.75% $2,594 $533,981 7% $2,661 $558,035 Keep in mind that most mortgage loans are amortized, meaning the total costs are calculated and then paid in even payments across the loan term. With these loans, you’ll pay more interest upfront and less toward the end of the term. For example, your first payment at 6% would see $2,000 go toward interest, while your final payment would have just $11.93. “At the beginning of the loan term, the majority of the monthly payment will go toward interest,” says Colleen Bara, a lending executive with Key Bank. “As the loan is paid down, more of the monthly payment is allocated toward the pay-down of the principal balance.” This means if you sell your home quickly after taking out your loan, you likely won’t have paid down your balance much—and may not make much from the home, profit-wise. If this is a concern, making an extra payment each year you’re in the house can help. “Make one extra principal payment yearly and you can shave off approximately seven years of interest,” Blanchard says.

Thursday, April 11, 2024 By: Ralph dibugnara Updated March 28, 2024 12:26 pm ET By Aly J. Yale https://www.wsj.com/buyside/personal-finance/mortgage-rates-01662579229 If you’re financing a home with a mortgage, ensuring you get the best possible rate is one of the smartest financial moves you can make. While it takes some legwork, the pay off is hard to argue with. Shaving even a fraction of a point from your rate can save you hundreds of dollars each month and tens of thousands over the life of the loan. For example, with a $400,000 mortgage, dropping from a 7% to a 6.5% rate would save you almost $50,000 in interest over a 30-year term—roughly enough to pay for a year of private college. Mortgage rates change constantly—and differ across mortgage companies . Here’s how to take advantage of those facts, compare current mortgage rates and get the best deal. Current mortgage rates: How high are average mortgage rates right now? For weeks now, average mortgage rates held steady in the high-6% range, according to Freddie Mac. As of the close of March, the average 30-year mortgage rate was 6.79%. Weekly mortgage rates WEEK ENDING AVERAGE 30-YEAR FIXED RATE AVERAGE 15-YEAR FIXED RATE March 28, 2024 6.79% 6.11% Mar. 21, 2024 6.87% 6.21% Mar. 13, 2024 6.74% 6.16% Mar. 7, 2024 6.88% 6.22% Feb. 29, 2024 6.94% 6.26% Freddie Mac “There has been a little more volatility since February, with rates moving up a bit—but they’re still below their highs from 2023,” says Rick Mount, managing partner of the Southwest region of Churchill Mortgage. Mount’s referring to last October, when rates nearly topped 8%. Still, average rates are about half a percentage point higher than they were a year ago—and borrowers have taken note. Applications for mortgages to purchase a new home are now down 16% compared to last year, according to the Mortgage Bankers Association. Refinances have dropped 9%. Where are mortgage rates headed? AVERAGE RATE DATE Current rate 6.79% March 28, 2024 This time last year 6.32% March 30, 2023 Highest point in last decade 7.79% Oct. 26, 2023 All-time high 18.53% Oct. 16, 1981 All-time low 2.65% Jan 7, 2021 Freddie Mac Mortgage rates have remained high thanks to stubborn inflation. Going into 2024, the Fed indicated lower rates may be on the horizon, but with inflation still sitting above the Federal Reserve’s 2% goal, those have yet to come to fruition. Instead, the Fed has kept interest rates elevated at its last several meetings, in an effort to bring inflation and consumer spending closer to its goal. “Inflation has continued to trend higher,’ says Ralph DiBugnara, a mortgage broker and senior vice president at Cardinal Financial, a mortgage company in Edgewater, N.J. “As long as inflation stays high or rises, the Fed will be hesitant to cut rates.” To be fair: The Fed doesn’t directly set mortgage rates, though they do tend to move in the same direction as the short-term rates it does control. As to when those rates might start to drop, it’s hard to say. Inflation notched up slightly in February, clocking in at 3.2%. “I believe the reality is we may see two to three cuts this year, all depending on inflation readings,” Mount says. “The Fed is committed to a 2% inflation rate, and I don’t expect we see meaningful cuts until that number is a reality.” According to the CME Group FedWatch Tool, which uses investing activity to predict future Fed moves, the Fed will likely hold steady on rates in May, with higher chances of rate cuts by the end of summer. MBA currently projects mortgage rates will drop to 6.3% by the end of the third quarter and 6.1% by year’s end. Fannie Mae predicts a 6.6% and 6.4% average, respectively. How are mortgage rates set? While the Fed influences mortgage rates, it is only one piece of the puzzle. Other external factors play a role, too—as do the details of your financial situation and loan choice. Here’s what you need to know about what determines your mortgage rate. External factors The overall state of the economy is a big contributor to the path of mortgage rates. When the economy is strong, rates tend to be higher. When the economy sputters, rates drop. “Interest rates often will rise or fall based on the strength of the economy, and ironically, bad news can be good news for lower interest rates,” says Bill Banfield, an executive at lender Rocket Mortgage. This is due in part to how economic conditions impact investment activity. When there are geopolitical concerns or the economy is wavering, investors tend to flock to safer investments—which include things such as Treasury bonds and mortgage-backed securities. This pushes the yields on those securities down (yields fall when bond prices rise), taking mortgage rates down with them. “When there is high demand for mortgage-backed securities, the prices of those MBS increase, which in turn can lower mortgage interest rates,” says Tanya Blanchard, founder of mortgage brokerage Madison Chase Capital Advisors. “This is because investors are willing to accept lower returns on their investments when the prices of MBS are high.” Finally, inflation factors in, too—and not just because of the Fed reaction. It also increases the costs for lenders to originate loans, which drives their prices higher as well. Personal factors Your personal finances will factor into your interest rate as well. First, there’s your credit score . Mortgage lenders use this number to gauge your risk as a borrower—or how likely you are to default on your loan. The lower your score, the higher the rate you’ll need to pay to compensate for the perceived risk. “Credit score is a very important consideration when applying for a mortgage,” Banfield says. “If someone has a proven track record of being responsible with their finances, they’ll be more likely to get a mortgage and a better rate.” The size of your down payment is important, too. A larger down payment means you have more to lose, which hopefully discourages you from defaulting. Smaller down payments, on the other hand, mean more risk for the lender and higher rates for you as a result. Loan-specific factors Last but not least, the type of mortgage loan you choose will also influence your rate. Loans backed by the government, such as Federal Housing Administration-backed FHA loans and Veterans Affairs-backed VA loans, tend to have lower rates than conventional or jumbo loans since they come with the federal government’s protection. Shorter-term loans (15 years, for example) also have lower rates than longer-term ones (30 years). As Goodwin explains, “While a shorter-term loan will come with a higher monthly payment, it could save you thousands on interest in the long run.” How, when and why to compare mortgage rates from different lenders Because every lender has different overhead costs, operating capacities and appetite for risk, mortgage rates can vary significantly from one company to the next. That’s why it’s important to consider several lenders before choosing where to get your loan. Freddie Mac recommends getting at least four quotes (it could save you an average of $1,200 a year , apparently). Just make sure you’re not only going by the rates a lender advertises on their website or on third-party sites. “Looking at advertised rates alone is not a good way to shop around,” Goodwin says. “Lenders typically display the lowest rates they offer as a headline to attract leads, but the actual rate you may be offered can vary dramatically depending on your own financial situation and the kind of loan you’re looking for.” Many advertised rates also include mortgage points —meaning you would need to pay an extra upfront fee to snag it. To get a rate that is truly a reflection of what you would pay as a borrower, you need to apply for preapproval . You’ll have to fill out an application and agree to a credit check for this. Once you’re done, you’ll get a loan estimate that will detail the total loan amount you are likely to qualify for, plus your interest rate and expected closing costs—or the fees required to originate, underwrite and close on your loan. Be sure to look at the APR, too—the annual percentage rate. This reflects the total annual cost of the loan, considering both your rate and any fees. Be warned, though: The rates you’re quoted aren’t guaranteed until you lock your rate. A rate lock guarantees your interest rate for a set period—usually only 30 to 60 days, depending on the lender. You’ll typically do this once you’ve found a home and have a contract in place. How to calculate your mortgage costs Comparing mortgage offers might seem tedious, but financially, it’s usually worthwhile. Even a small change in rate can have a big impact on your monthly payment and long-term interest costs. You can use a mortgage calculator to break down the exact costs or use your loan estimate. This should detail your monthly payment, your interest rate and your total interest paid in five years. See the difference that incremental rate changes can make on the cost of a 30-year, $400,000 home loan below: RATE MONTHLY PAYMENT INTEREST OVER 30 YEARS 5% $2,147 $373,023 5.25% $2,208 $395,173 5.50% $2,271 $417,616 5.75% $2,334 $440,344 6% $2,398 $463,352 6.25% $2,462 $486,632 6.50% $2,528 $510,177 6.75% $2,594 $533,981 7% $2,661 $558,035 Keep in mind that most mortgage loans are amortized, meaning the total costs are calculated and then paid in even payments across the loan term. With these loans, you’ll pay more interest upfront and less toward the end of the term. For example, your first payment at 6% would see $2,000 go toward interest, while your final payment would have just $11.93. “At the beginning of the loan term, the majority of the monthly payment will go toward interest,” says Colleen Bara, a lending executive with Key Bank. “As the loan is paid down, more of the monthly payment is allocated toward the pay-down of the principal balance.” This means if you sell your home quickly after taking out your loan, you likely won’t have paid down your balance much—and may not make much from the home, profit-wise. If this is a concern, making an extra payment each year you’re in the house can help. “Make one extra principal payment yearly and you can shave off approximately seven years of interest,” Blanchard says.